The seasonal factors that our researchers at the Philadelphia Fed use to calculate the survey's diffusion indexes were affected by atypical patterns because of the onset of the pandemic one year ago. For several variables, revised seasonal factors shifted by much more than is normal. We may revise our seasonal adjustment approach after further investigation.

Note: Survey responses were collected from March 8 to March 18.

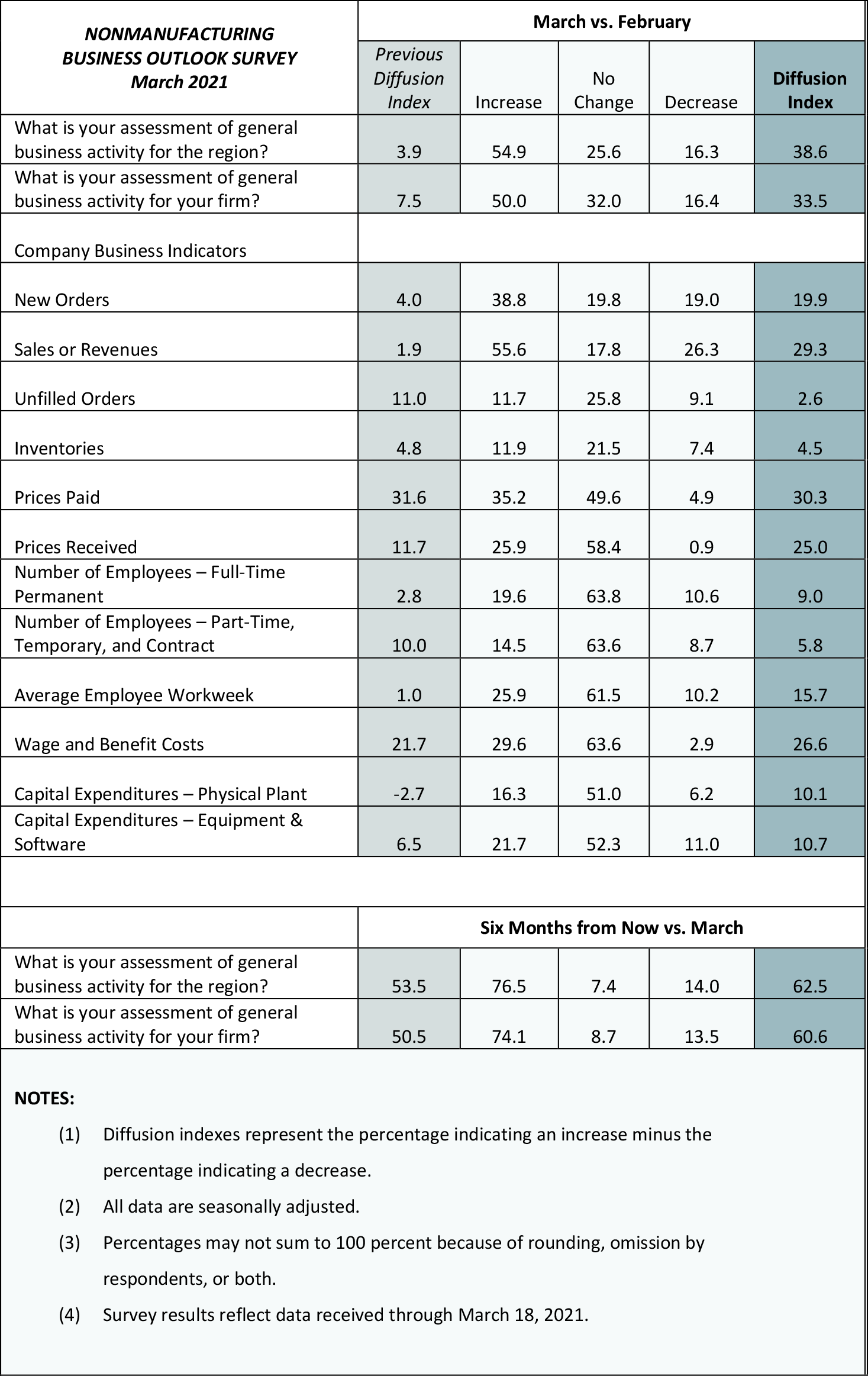

Responses to the March Nonmanufacturing Business Outlook Survey suggest expansion in nonmanufacturing activity in the region. The indexes for general activity at the firm level, sales/revenues, and new orders all posted gains. Additionally, the index for full-time employment increased. The firms continued to report overall increases in the prices of both their own goods and their inputs. The respondents continued to anticipate growth over the next six months.

Current Indexes Improve

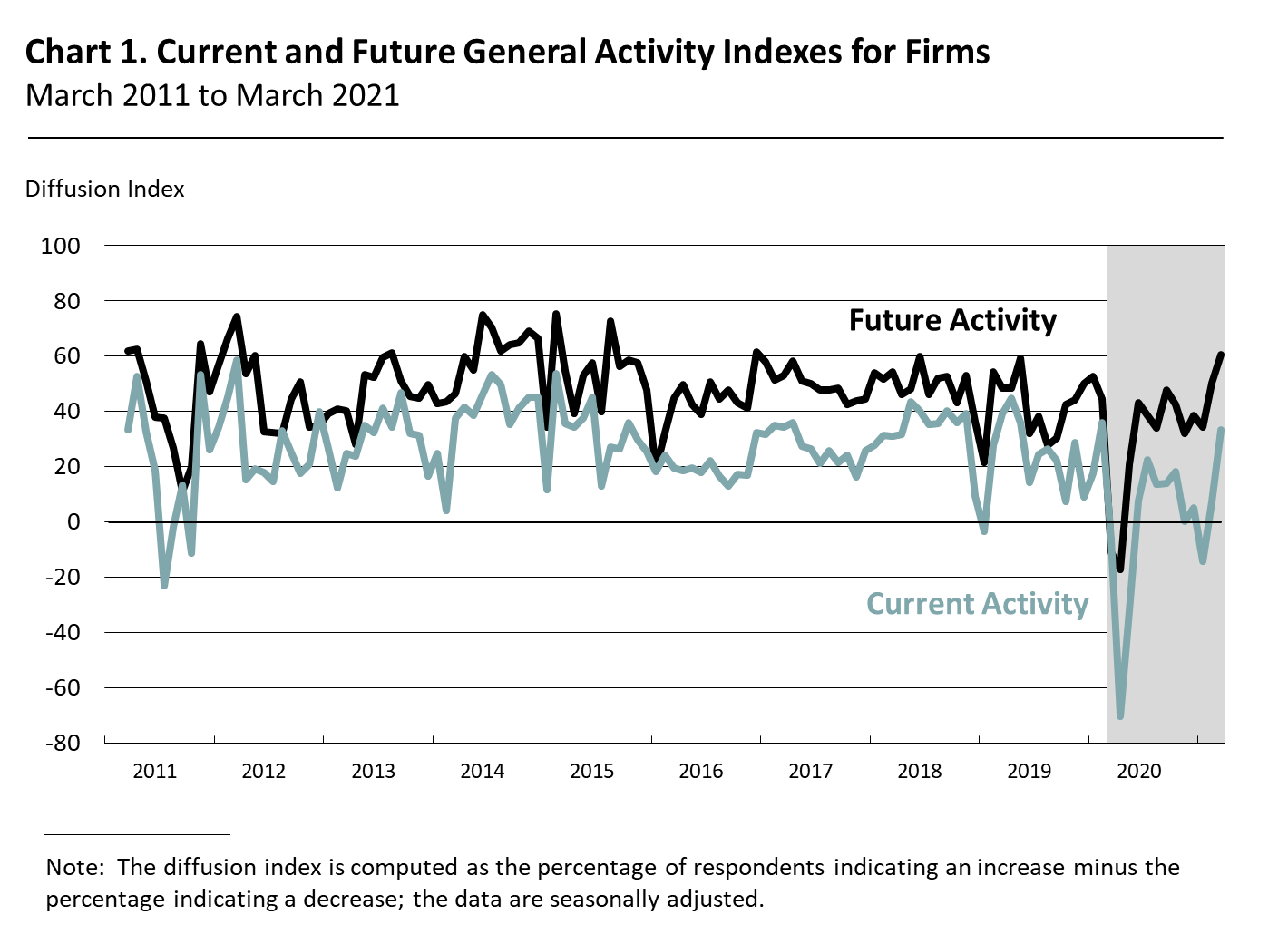

The diffusion index for current general activity at the firm level rose 26 points to 33.5 in March, its highest reading since February 2020 (see Chart 1). Half of the firms reported increases in activity (up from 33 percent last month), and 16 percent reported decreases (down from 26 percent). The new orders and sales/revenues indexes also registered their highest readings since February 2020: The new orders index increased 16 points to 19.9, and the sales/revenues index rose 27 points to 29.3. Nearly 56 percent of the responding firms reported increases in sales/revenues (up from 32 percent last month), while 26 percent reported decreases (down from 30 percent). The regional activity index rose 35 points to 38.6.

Firms Report Overall Increases in Employment

The full-time employment index rose from a reading of 2.8 in February to 9.0 in March. Nearly 64 percent of the firms reported steady full-time employment levels, while the share of firms reporting increases (20 percent) was higher than the share reporting decreases (11 percent). The part-time employment index fell 4 points to 5.8, while the wages and benefits indicator increased 5 points to 26.6. The average workweek index rose 15 points to 15.7.

Respondents Continue to Report Overall Price Increases

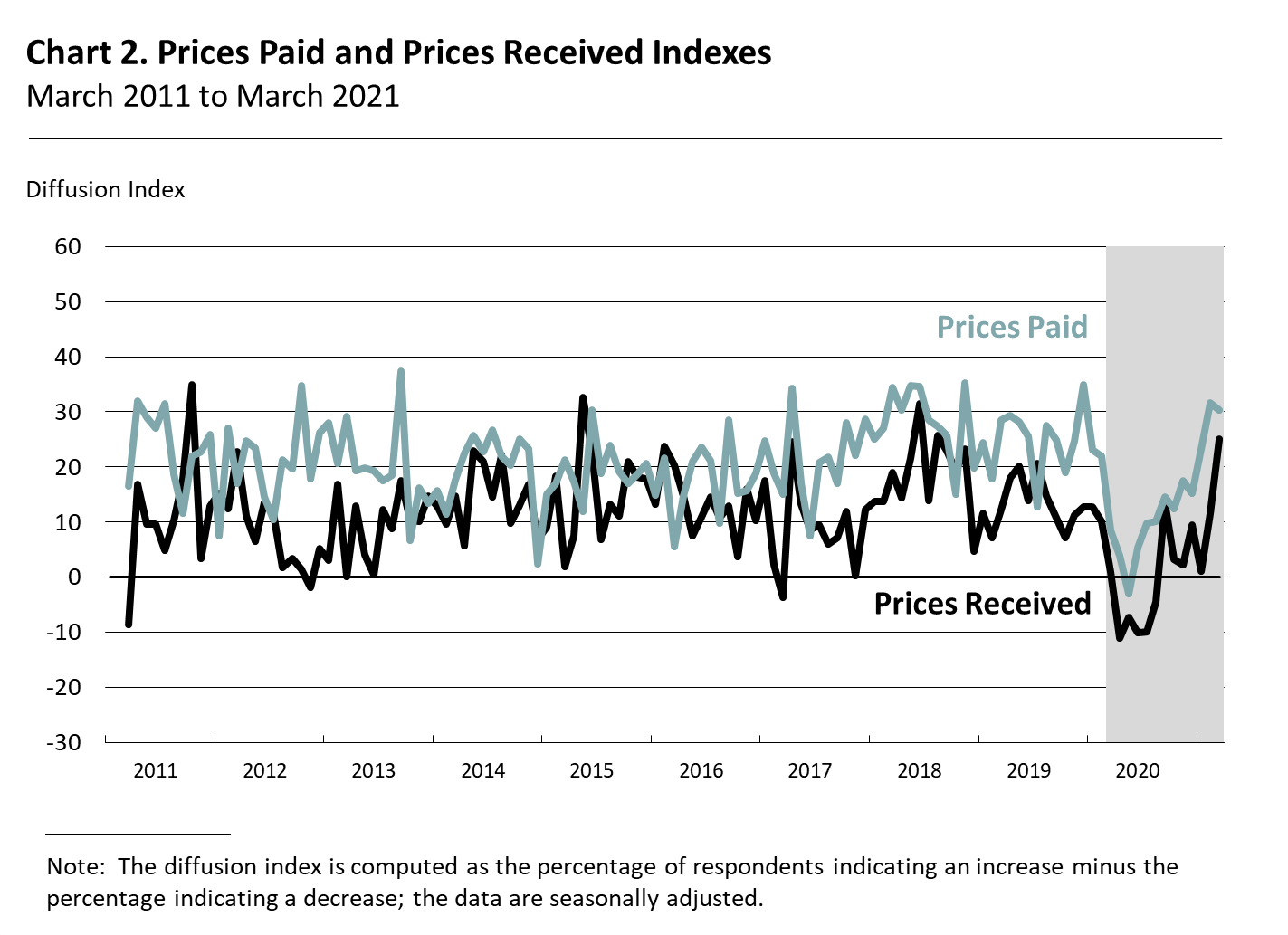

The prices paid index edged down 1 point to 30.3 (see Chart 2). Over 35 percent of the respondents reported increases, and only 5 percent reported decreases. Half of the respondents reported stable input prices. Regarding prices for firms' own goods and services, the prices received index increased from a reading of 11.7 in February to 25.0 in March. The share of firms reporting increases in prices received (26 percent) far exceeded the share reporting decreases (1 percent). More than 58 percent of the firms reported no change in prices for their own goods and services.

Firms Report Some Difficulties Finding Workers

In special questions this month, the firms were asked generally about worker shortages, any perceived mismatches between skill requirements and labor supply, and the ways in which they were dealing with these problems (see Special Questions). Twenty percent of the firms indicated labor shortages, while 23 percent indicated skills mismatches between requirements and available labor. Over 21 percent of the surveyed firms also reported that they had positions that have remained vacant for more than three months. A sizable share of firms (33 percent) reported that they were not hiring at the moment, while few firms (6 percent) reported seeing a broad labor shortage, such that it is hard to fill any position. The firms have adopted a mix of strategies to deal with these problems, including stepping up recruiting efforts and increasing training of existing employees and new hires.

Firms Continue to Anticipate Growth

Both future activity indexes suggest that firms continue to anticipate growth over the next six months. The diffusion index for future activity at the firm level rose from a reading of 50.5 in February to 60.6 this month (see Chart 1). Over 74 percent of the firms expect an increase in activity at their firms over the next six months, compared with 14 percent that expect decreases and 9 percent that expect no change. The future regional activity index increased 9 points to 62.5.

Summary

Responses to this month's Nonmanufacturing Business Outlook Survey suggest expansion in nonmanufacturing activity in the region. The indicators for firm-level general activity, new orders, and sales/revenues all increased. Additionally, firms continue to report overall increases in prices and employment. Overall, the respondents continue to expect growth over the next six months at their own firms and in the region.

Special Questions (March 2021)

|

|

Percent (%)

|

1. Has your firm experienced any significant labor shortages or mismatch between labor skill requirements and labor supply? (Check as many as apply)*

|

|

Labor shortages

|

20.0 |

|

Skills mismatch |

22.5 |

|

Job vacancies remaining more than three months |

21.3 |

| |

2. Is your firm experiencing a labor shortage in general or in certain skills, abilities, or positions?

|

|

We are hiring and receive a sufficient number of qualified applicants to fill open positions.

|

17.5 |

|

We are seeing a significant shortage in qualified applicants for some skills and positions.

|

12.5 |

|

We are seeing a tightening labor market, such that it is getting harder to fill positions in general, but still possible to fill them.

|

18.8 |

|

We are seeing a broad labor shortage, such that it is hard to fill any position.

|

6.3 |

|

We are not hiring.

|

32.5 |

|

Not applicable

|

3.8 |

|

No response

|

8.8 |

| |

3. What actions has your firm taken to address skills shortages?

(Check as many actions as apply)*

|

| Increased recruitment efforts |

26.3 |

| Provided additional training to existing staff |

23.8 |

| Increased wages |

20.0 |

| Increased training for hired workers |

15.0 |

| Have hired less qualified workers to meet labor requirements

|

11.3 |

| Increase benefits |

7.5 |

| Expand recruitment outside of the region

|

6.3 |

| Other |

6.3 |

| Partner with educational institution to align curriculum with talent needs |

5.0 |

| Phased retirement program to retain older workers |

5.0 |

| Increase recruitment incentives |

3.8 |

| Decreased production |

2.5 |

| *Percentage will not add to 100 because more than one action could be selected. |

Summary of Returns (March 2021)